Accept Payments.

Grow Your Business.

Transparent pricing, zero hidden fees, and dedicated support. Credit card processing with rates as low as 0% for businesses across all 50 states.

30+

Years Experience

50

States Covered

96%

POS Compatible

Zero Cost Processing

Pass processing fees to customers and keep 100% of every sale.

Interchange Plus Pricing

Transparent pricing with no markups. Pay only what the card networks charge.

No Long-Term Contracts

Month-to-month service with no cancellation fees or hidden commitments.

Fast & Easy Setup

Get approved and processing payments in as little as 24 hours.

What We Do

Payment Solutions Tailored to Your Business

From credit card processing and cash discount programs to POS systems and digital marketing, Valiant Payments delivers comprehensive solutions that help your business save money and grow.

Credit Card Processing

Accept all major credit cards (Visa, Mastercard, Amex, Discover) with secure, fast transactions and next-day funding.

Learn More

Cash Discount Program

Reduce processing fees to 0% with our fully compliant cash discount solution.

Learn More

POS Systems & Terminals

State-of-the-art Clover and Valor terminals designed for speed, reliability, and ease of use.

Learn MoreOur Products

Best-in-Class Payment Terminals

Choose from industry-leading Clover and Valor terminals designed for speed, reliability, and ease of use. Every device comes pre-configured and ready to process from day one.

Clover Station Duo

14" merchant display with customer-facing screen, receipt printer, and cash drawer — the ultimate countertop POS.

View Details

Clover Station Solo

14" swivel touchscreen with fingerprint reader, receipt printer, and powerful cloud-based POS platform.

View Details

Clover Mini

Compact 7" touchscreen POS with built-in printer — big capabilities in a small footprint.

View Details

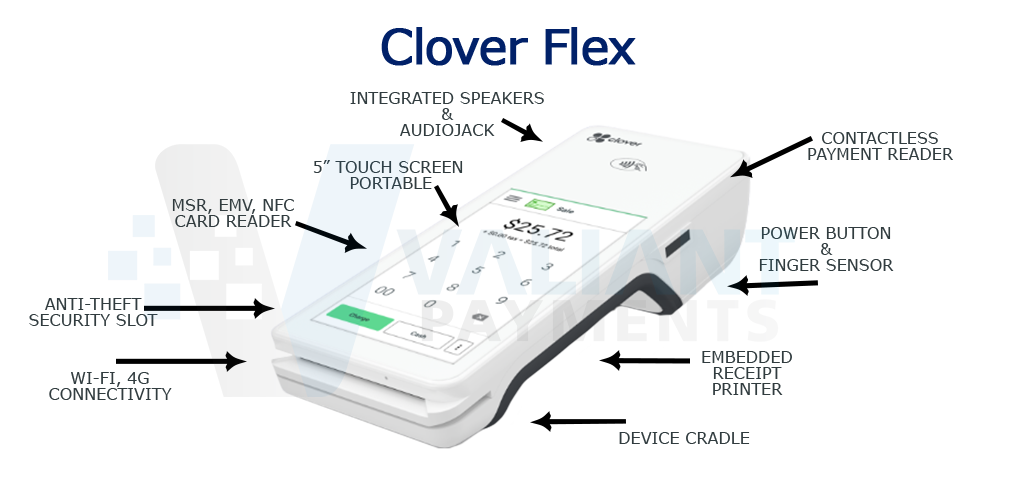

Clover Flex

Portable 5" handheld POS with 8-hour battery, barcode scanner, and built-in printer for payments anywhere.

View Details

Clover Go

Ultra-portable Bluetooth card reader that pairs with your smartphone or tablet for payments on the go.

View Details

Valor VL500

5.5" handheld Android terminal with pay-at-table, bill splitting, smart tipping, and cash discount built in.

View Details

Valor VL100

Countertop POS terminal with large touchscreen, versatile connectivity, and built-in cash discount support.

View Details

QuickSale Q2

Lightweight 5.5" handheld terminal with 12+ hour battery, integrated printer, and QuickBooks integration.

View DetailsPricing

Transparent Pricing, Real Savings

See how much you could save with Valiant Payments. No hidden fees, no long-term contracts, no surprises.

Industry Average

Based on $20,000/mo volume

~$6,336/year

- Standard processing rates

- Long-term contracts

- Hidden fees common

- Limited support

Zero Cost Processing

Based on $20,000/mo volume

~$780/year

- 0% processing fees

- No long-term contracts

- Free terminal included

- Dedicated account manager

- Next-day funding

- Free marketing services

Interchange Plus

Based on $20,000/mo volume

~$3,971/year

- Transparent interchange rates

- No long-term contracts

- Next-day funding

- Dedicated account manager

- Online reporting dashboard

Industries We Serve

Solutions for Every Business

From restaurants and retail to healthcare and field services, we provide customized payment solutions built for the unique demands of your industry.

Restaurants & Bars

High-speed payment processing with pay-at-table, bill splitting, and smart tipping designed for food and beverage.

Learn MoreRetail & E-Commerce

Inventory management, customer loyalty tracking, and omnichannel payment solutions for modern retail.

Learn More

Healthcare

HIPAA-compliant payment solutions with recurring billing, patient payment plans, and secure data handling.

Learn More

Auto & Dealerships

Large-ticket transaction processing with parts inventory management, service scheduling, and multi-location support.

Learn More

Hospitality

Payment solutions for hotels, resorts, and event venues with mobile check-in, room charging, and loyalty programs.

Learn More

HVAC & Field Services

Mobile payment processing for on-site work with invoicing, recurring billing, and GPS tracking.

Learn MoreReady to Lower Your Processing Costs?

Join thousands of businesses that trust Valiant Payments for transparent, affordable credit card processing. Get a free quote today.